PLANNING FOR YOUR FAMILY, BUSINESS, AND ESTATE

Succession, Without All the Drama

INTRODUCTION

A Thoughtfully Structured Succession Plan Ensures the Viability of Your Business and the Security of Your Family: Presenting Addicus Optimized Continuity Strategy

Business is your family. Family is your business. For you, one without the other doesn’t exist. And though running a family business has its own set of challenges, you (on most days) wouldn’t have it any other way.

Keeping your business running smoothly and ensuring everyone is focused on its growth and profitability, is why having the right continuity strategy in place is essential.

Addicus works with our family business-owning clients to build an Optimized Continuity Strategy (OCS), based solidly on three pillars of planning:

In the following pages, we provide a more detailed explanation of the elements that comprise these pillars, and some opinion-driven thoughts from the firm – enabling you to review some of the many ways to structure your plan. While every client’s plan is different, our goal remains the same: To deliver the Optimized Continuity Strategy that works best for your business – and your family.

BUSINESS SUCCESSION PLANNING

Pillar I: Business Succession Planning

Business succession is never devoid of challenges. Especially since many family businesses are comprised of a mix of stakeholders. Below, we delve a bit deeper into these groups and some of the key decisions you may need to consider regarding each one.

Operating Family Members

If you are intent on family succession and have identified (or are intending to identify) the next generation of management from within your family ranks, it is important to have a plan in place that will:

- Ensure uninterrupted business operations

- Provide clarity for all family members

- Present the right optics to both family and non-family employees

It should go without saying, but it is worth repeating: The more seamless your transition, the greater success you can expect.

With that in mind, you can also expect we will counsel you – and help you:

Name a family member(s) as “successor manager” to avoid the sometimes-irreparable damage done when an unplanned transition leads to a literal stoppage of business while operating decisions, ownership disputes, and family squabbles are sorted out in the probate court system. You do not want an executor/executrix, trustee, or judge impeding or stopping your ability to run the business and grow prosperity for all stakeholders.

Evaluate the real-time “readiness stage” your chosen successor possesses. Consider the optics

of naming that successor, and how that decision will be perceived by other family members and non-family employees. Contemplate how to best support, train, and socialize this person throughout the organization so they are seen as having “earned it” – moving this decision (with as much velocity as possible) from acknowledgment to acceptance, and ultimately enthusiasm. Make sure the chosen successor fully appreciates the challenge and burden of being chosen and is ready to do their part

to earn and command the respect and trust needed to be successful.

Create and/or update operating agreements to ensure control is structured properly, and there are checks and balances in place. Confirm that transfer of that control is clearly defined and legally unimpeachable (which also means ensuring legal documents are drawn up by attorneys who are subject matter experts and not developed based on online forms that can lead to substandard protections and substantial financial burdens in terms of legal exposure and fees down the road).

In fact, it is often the case that when we review existing documents, key stakeholders have no idea what they have bound themselves to and what the implications of those agreements might be in various situations. Also, it is important that the senior generation clearly conveys their resolve and comfort with the decision to name a successor, but also explains the rationale and gains buy-in from family and non-family stakeholders and management.

Develop an iron-clad estate plan, along with all relevant legal documents, that codify your go-forward intentions for the enterprise – and review these documents at least once a year to refamiliarize yourself and ensure any changes in your desires are incorporated and that all elements remain in compliance with frequently changing laws and regulations.

Non-Operating Family Members

In situations where non-operating family members are also owners in closely held businesses, we have witnessed the fraying of (and long-lasting damage to) family relationships when succession decisions are made, and emotions come into play.

The familiar saying – “Fair is not equal and equal is not fair!” – becomes very much the refrain in these instances and, when this sometimes leads to disruptive behavior, steps must be taken for the sake of the business and the greater family.

When working with you to decide if designing a buyout is the right course of action, we are also there to help you navigate the issues that go beyond the complexion of the actual buyout agreement. This can be a very sensitive emotional landmine to navigate and may remind you of playing 3D chess. You should stop and ensure you have the proper appreciation for the gravity of some of the discussions and decisions that might unfold and carefully plan your moves to drive the best outcome.

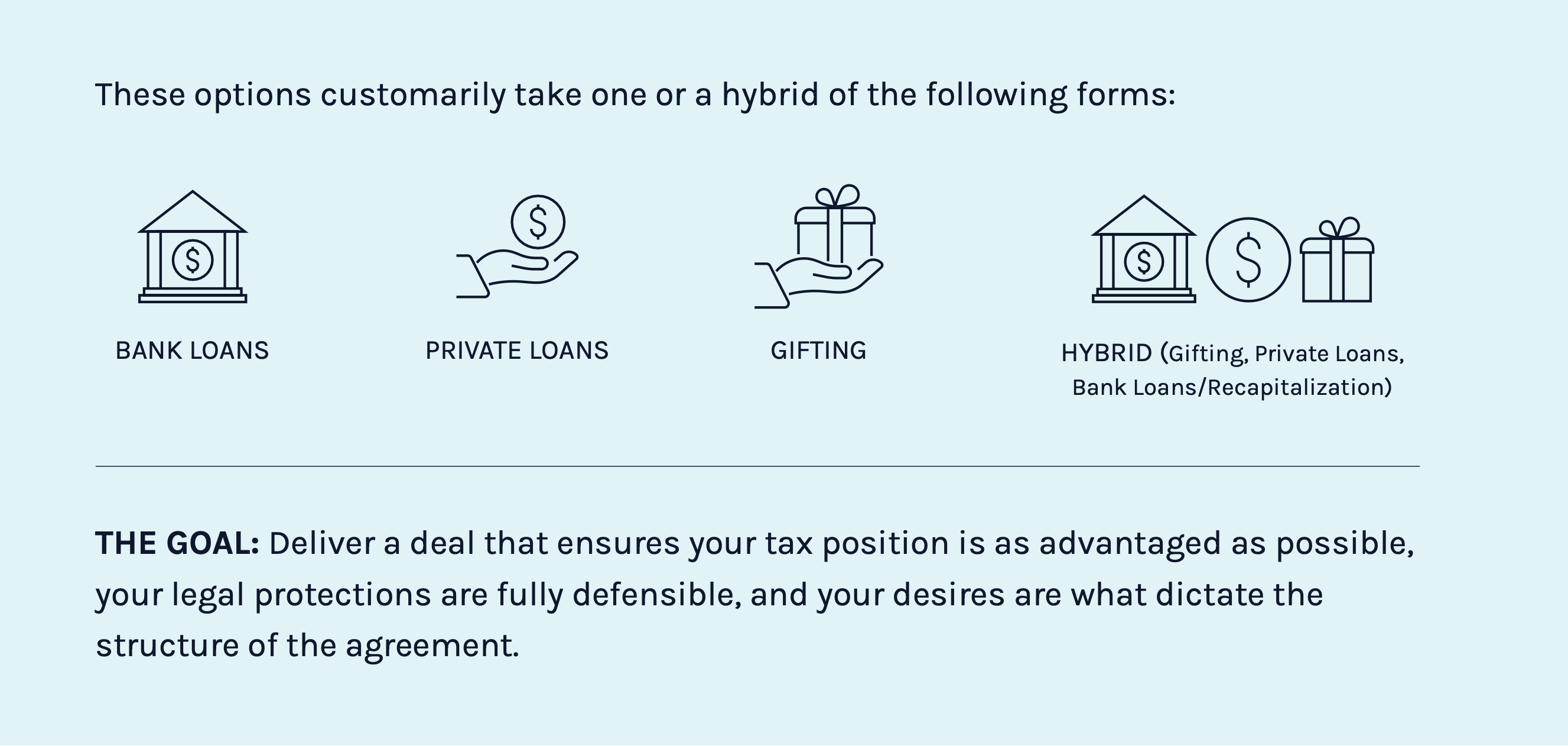

These issues include any tax implications arising from “related party tax rules” as well as the impact your corporate structure (C-Corp, S-Corp, Partnership, Trust, Ownership, etc.) has on the final buyout agreement. As with all buyout agreements, there may be limitations on funding structure (whether privately or commercially financed), and we work to provide you with the most desirable options.

Non-Family Management

When a key non-family manager (or management team) is a material contributor to company stability, a driver of growth, and/or essential to the support/success of your company’s next generation of family management, we often recommend retention plans that provide controlled, restricted, or synthetic ownership. Ideally, we do not like to see closely-held family businesses have non-family-holding voting equity.

To that end, there are a variety of options to consider, and we work with you to ensure all parties view any plan complexion to be mutually beneficial:

Pillar II: Family Governance

Governance is all about preparation. This includes preparing for eventual certainties, such as retirement and death. It also includes being ready for other situations (disability, forced exit, dispute resolution), that generally seem to occur at the most inopportune times (Murphy’s Law).

Being able to deal with a situation actively, versus being caught flat-footed, requires the right combination of knowledge and planning.

Death

If there is an existing plan in place, it is most commonly one established to address the passing of the company owner(s)/leader(s). If this plan is a traditional buy/sell agreement, the next steps will often be activated upon death and usually addressed in the form of life insurance and/or an estate plan. Many plans include some combination of both. That said, on the life insurance side, it is good to remember:

Life insurance is not always easy to acquire

Term life is a temporary (and often not complete enough) fix

Life insurance policies must be structured with extreme care

There can be negative tax implications depending on the ownership, funding, and death benefit recipients associated with life insurance policies.

Disability

Disabilities manifest in two forms: cognitive and physical. Truth is, if we live long enough, we will all be afflicted by at least one of these disabilities. As a business, especially one that includes the emotional component of being family-run, it is important to consider your options:

Long-term care insurance

Short/Long-Term Disability Income Insurance

Disability buyout provisions

Specialized insurance products

It is vitally important to have clear disability provisions in the governing documents that are tightly defined – including potential mandated medical testing stipulations when cognitive disability is suspected, clear definitions of what it means to be disabled, and other checks and balances. You want to avoid “disability,” provisions ever being used in subversive or coercive ways. An up-to-date Business Continuity Plan should be in place to smoothly continue operations after the incapacitation of the owner/leader.

Retirement

While it seems like the conditions under which an active family member can retire should be defined from day one, many companies put this planning off until it presents itself with a level of urgency for which no one is prepared.

Along with being ready for the inevitability of retirement of family leaders/owners, defining what it takes to qualify for retirement, and how family member retirements will be funded, are essential decisions to have firmly in place.

Dispute Resolution

There is nothing more disheartening than family members facing off in court. In addition to the inter-family turmoil it ferments, it is a financial burden on every family member involved – as well as every trustee, business manager, and entity that must seek legal counsel, which can run the cost completely out of control. What's more, corporate structure, especially in family-run businesses, can lead to major issues once it makes its way into the courts. Further, the embarrassment of airing the family’s dirty laundry publicly can lead to lasting family damage in the business and community.

For these reasons and others, we strongly advise our clients to consider forced mediation and cooling-off periods as the path to dispute resolution. In our experience, it is the quickest way to a favorable outcome for the business and remaining family members. As the least contentious form of dispute resolution, it is also the best way to maintain as much respect and understanding as possible in a situation where family members are at odds. Further, consider a forced but orderly sale of the business as a potential provision that dissuades the family members from fighting over control of the business. Put in place salary and distribution policies for the operating family members to ensure fair compensation for services, and continued cash flow distributions.

Forced Exit

Unfortunately, there are times when the removal of a member – be they an employee, shareholder, board member, or other stakeholder – must be undertaken for the good of the enterprise. In preparation for this potential scenario, a plan that considers under what circumstances a forced exit may be executed, how to ensure fairness, and how to avoid legal conflict should be in place.

Board of Directors

As a family business, you are not compelled to form a formal board – especially if family members will retain complete management control. In fact, many family businesses install a less formal “board of advisors” as an alternative to, a formal, controlling board, especially one with outsiders holding seats. However, if you feel a board might be right for your business, here are just a few pieces of advice we always share:

Consider a manageable board size, perhaps a maximum of 5 board members

Seek members who will ensure you benefit from both industry and non-industry expertise and perspective

Ensure a defined set of checks & balances are codified and in place

Pillar III: Tax & Estate Planning

This third pillar of your Optimized Continuity Strategy is one that controlling generations often neglect until they can’t – which never results in the best possible outcome.

Regardless of how simple or complicated your tax & estate profile may be, having an updated plan in place is foundational to ensuring the wishes you have for the business and your family are executed as you desire. Your tax & estate planning partner should first and foremost:

We would recommend that you find competent counsel who will intently listen to your desires, give you wise counsel about options, but at the end of the day, be willing to take the professional risk of providing an informed, but still opinionated recommendation. It does no good to get nothing but education on the voluminous options without some guidance on which options make the most sense, having understood the issues and desires/objectives.

Perhaps the most important advice, next to having your planning in place, is that you review those plans with a professional on a regular basis to ensure the plan you developed yesterday is aligned with not only your desires but the laws and regulations as they stand today.

Conclusion

Bringing the three pillars of thoughtful succession planning together in an Optimized Continuity Strategy ensures the plans you have for the next phase of your family business – and the wishes you have for family members – are thoughtfully integrated into a single, thoughtfully-integrated plan.

This enables you, and everyone involved, to stay focused on building your family business, maintaining and growing the family’s prosperity and your overall Family Wealth Enterprise (FWE).

It also enables you to enjoy the one of the most valuable planning benefits of all: Peace of mind.

This material has been prepared by Addicus Capital Advisors in better understanding transactions of the type described herein. The market trends, data, industry analysis and corresponding discussions set forth in this material are based upon information provided by third party sources. Addicus Capital Advisors has not assumed any responsibility for independently verifying the accuracy of such information and disclaims any liability with respect to the information herein.

This material, and any advice Addicus Capital Advisors may provide to you, may include certain forward-looking statements that are based on our beliefs and assumptions about certain companies, markets or industries, and on information currently available to us.

Forward-looking statements include all statements that are not historical facts and can be, but are not always, identified by the use of forward-looking terminology such as the words “believes,” “expects,” “anticipates,” “intends,” “plans,” “estimates,” “may”, “will” or similar expressions. Forward-looking statements involve risks, uncertainties and assumptions. Actual results or outcomes may differ materially from those expressed in these forward-looking statements. You should not put undue reliance on any forward-looking statements, and no forward-looking statements can be guaranteed.

You should understand that many important factors, in addition to those discussed herein, could cause forward- looking statements about a business, market or industry to ultimately be incorrect. These factors include, but are not limited to, (i) legal and regulatory risks and uncertainties, including changes in the laws, rules and regulations, (ii) changing competitive environments, (iii) changes in personnel or management within particular companies, (iv) technological change, (v) economic, political and other market conditions, and (vi) inaccuracies in our analysis of risks, factors and uncertainties or the ability of particular companies, markets or industries to develop strategies to deal with them.

Past trends and performance are not guarantees of future market activity, deal terms or performance; accordingly, Addicus Capital Advisors makes no representation, warranty or guaranty regarding any particular offer, deal term or transaction, or the outcome of or any returns related to any of the foregoing.

The analysis and discussion set forth in this material is general and intended for informational purposes only. It is not, and is not intended to be, investment advice. In any case, Addicus Capital Advisors is not making any representation regarding the suitability of any business, investment or financial decision for your particular circumstance, and any such decision should be made independently by you in consultation with your tax, financial and other legal advisors. Further, any advice we may provide is qualified in its entirety by our limited knowledge of the relevant facts and circumstances of your situation, and only represents a reasonable interpretation of currently available information, including without limitation the language of the relevant provisions of the Internal Revenue Code of 1986, as amended, and regulations and administrative guidance issued by the Department of the Treasury. Any advice we may ultimately provide is subject to change based on further administrative interpretations or the availability of additional information.

This material is provided as of the date hereof, and Addicus Capital Advisors assumes no obligation to update it or correct any information herein. This material is the property of Addicus Capital Advisors and is provided to you on a confidential basis. Absent Addicus Capital Advisors’ prior written consent, this material, whether in whole or in part, may not be copied, photocopied, or duplicated in any form by any means, or redistributed.